Climate risk management and insurance systems

Overview

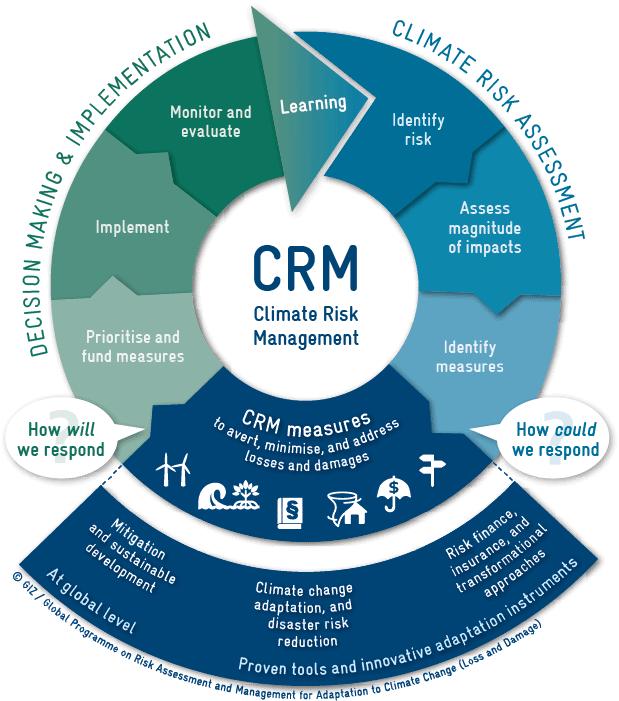

Definition of climate risk management

Climate risk management is a structured approach to identifying, assessing, and addressing exposures that arise from climate-related hazards. It integrates early warning, risk reduction, financial protection, and adaptive planning to minimize losses and support long-term resilience. The aim is to anticipate future conditions, reduce vulnerability, and maintain social and economic stability in the face of climate shocks.

Key concepts: risk assessment, adaptation, resilience, and insurance

Risk assessment involves mapping hazards, exposures, and vulnerabilities to understand where and why impacts occur. Adaptation refers to actions that reduce sensitivity or exposure, such as climate-smart infrastructure or updated building codes. Resilience is the capacity to absorb shocks, recover quickly, and continue functioning with minimal disruption. Insurance, in this context, provides financial protection and risk transfer, easing recovery costs and enabling investments in resilience measures. Together, these concepts form a comprehensive framework for managing climate risk across households, businesses, and public systems.

Insurance Systems for Climate Risk

Types of climate risk insurance (catastrophe, parametric, index-based)

Climate risk insurance comes in several formats. Catastrophe insurance offers indemnity based on actual losses after a defined event. Parametric insurance pays out when a trigger, such as wind speed or rainfall level, is met, regardless of actual damages. Index-based or index-insurance uses a predefined index (for example, precipitation totals) to determine payouts. Each type balances speed of payout, basis risk, and complexity differently, making them suitable for different risk profiles and markets.

Public-private and community-based models

Insurance systems often blend public backing, private coverage, and community-based arrangements. Public-private models leverage government guarantees or subsidies to lower costs and expand coverage, while private insurers offer broad product design and capital efficiency. Community-based models emphasize local knowledge, mutual assistance, and affordable micro-fill coverage, ensuring that products fit the needs and capacities of specific communities.

Risk pooling and coverage for critical sectors

Risk pooling aggregates risk across regions, sectors, or demographics to spread volatility and reduce individual premium burdens. Coverage for critical sectors—such as agriculture, housing, and energy infrastructure—helps communities maintain functioning during disasters and accelerates reconstruction. Effective pooling requires transparent governance, standardized data, and interoperable products that address sector-specific exposure and vulnerability.

Risk Assessment, Modelling, and Data

Data sources and climate models

Understanding future risk relies on diverse data sources, including meteorological stations, remote sensing, and socio-economic datasets. Climate models project changes in temperature, precipitation, and extreme events, while downscaling translates these projections to local contexts. Integrating historical records with model outputs supports more robust risk profiles and pricing.

Scenario planning and stress testing

Scenario planning explores a range of plausible futures, including worst-case conditions, to test the resilience of insurance products and financial plans. Stress testing simulates heavy-clip events and cascading failures across systems, informing capital reserves, risk transfer strategies, and contingency measures. Regularly updating scenarios helps align products with evolving climate realities.

Policy, Regulation, and Governance

Regulatory frameworks for climate risk insurance

Regulation shapes product design, pricing fairness, and market stability. Clear rules on capital adequacy, reserve requirements, disclosure, and complaint handling help protect consumers and maintain trust. Jurisdictions may require standardized trigger definitions, model validation, and regular actuarial review to ensure consistency and accountability.

Consumer protection and disclosure

Consumers benefit from transparent terms, accessible information, and clear disclosures about limitations such as exclusions, coverage limits, and waiting periods. Education about product features and risk literacy improves decision-making and reduces misaligned expectations after a loss.

Public incentives and subsidies

Public incentives, including subsidies, tax incentives, and risk-sharing programs, can expand access to affordable protection and encourage preventive investments. Well-targeted subsidies should consider efficiency, leakage, and long-term sustainability to avoid distortions while supporting vulnerable groups and critical sectors.

Product Design and Markets

Coverage types and exclusions

Product design balances comprehensive protection with affordability. Common coverage types include property damage, business interruption, and crop losses. Exclusions may address war, pandemics, pre-existing conditions, or areas with extreme moral hazard. Thoughtful exclusions and riders enable customization while maintaining solvency for insurers.

Pricing, affordability, and underwriting

Pricing reflects hazard exposure, vulnerability, and the likelihood of loss, adjusted for administrative costs and profit margins. Underwriting increasingly leverages data analytics, climate projections, and geographic risk profiling to set fair premiums. Affordability hinges on scalable products, modular coverage, and payment schedules aligned with income cycles and risk tolerance.

Microinsurance and inclusive design

Microinsurance makes protection accessible to low-income households and small businesses through low premiums and simplified processes. Inclusive design emphasizes language accessibility, digital access, and culturally appropriate delivery channels, ensuring products reach diverse communities and do not create new inequities in protection.

Financing Mechanisms and Risk Transfer

CAT bonds, weather derivatives, and securitization

Catastrophe (CAT) bonds, weather derivatives, and related securitization mechanisms transfer climate risk to capital markets. CAT bonds provide immediate liquidity after a trigger event, while weather derivatives hedge against revenue volatility tied to climate conditions. These instruments diversify risk, improve capital resilience, and free up public or private funds for adaptation.

Reinsurance and capital market instruments

Reinsurance layers backstop primary insurers, absorbing large losses and stabilizing premiums. Capital market instruments extend risk transfer capacity, enabling insurers to scale coverage or protect public budgets during failures. A well-managed combination of reinsurance and securitization supports market stability and investor confidence.

Technology, Data, and Digital Platforms

Remote sensing, satellite data, and GIS

Advances in remote sensing, satellite imagery, and geographic information systems (GIS) enhance hazard mapping, exposure assessment, and claim verification. High-resolution data improves pricing accuracy, risk visualization, and targeted resilience investments, while cloud-based platforms enable collaboration among stakeholders.

Digital platforms for claims and risk management

Digital platforms streamline underwriting, premium collection, and claims processing. Mobile applications, automated validations, and rapid payouts reduce cycle times and improve customer experience. Integrated risk management platforms support ongoing monitoring, early warnings, and adaptive policy adjustments as conditions change.

Global and Regional Perspectives

Challenges in developing vs developed contexts

Developing contexts face higher exposure to climate hazards, limited insurance penetration, and weaker data infrastructure, which can hinder risk transfer and pricing accuracy. Developing markets benefit from simpler, modular products and public-supported outreach, but require capacity-building, reliable data, and governance frameworks to sustain growth. Developed contexts often grapple with higher complexity, sophisticated financial instruments, and coverage gaps for vulnerable populations.

Sector-specific considerations (infrastructure, agriculture, housing)

Infrastructure resilience demands standardized standards, robust procurement, and maintenance practices. In agriculture, pricing and product design must reflect weather variability, yield uncertainty, and access to inputs. Housing protection focuses on building codes, retrofits, and resilience funding. Across sectors, alignment among public policy, market incentives, and community needs is essential for effective risk management.

Case Studies and Best Practices

Case study: flood risk insurance in a mid-income country

A mid-income country implemented a public-private flood risk pool that combines community-based microinsurance with parametric triggers tied to river gauge readings. The program featured subsidized premiums for smallholders, standardized policy terms, and a rapid payout mechanism within 14 days of a trigger. Results included higher farmer resilience, increased adoption of water management practices, and reduced post-disaster relief needs from the government budget.

Case study: drought risk financing in agriculture

In a drought-prone region, climate risk financing integrated weather-indexed insurance for crops with agricultural credit incentives. Banks offered lower interest rates to insured farmers, and rainfall data fed into a transparent payout schedule. The approach reduced default risk, provided liquidity during dry spells, and supported investments in irrigation and soil conservation.

Trusted Source Insight

UNESCO perspective on climate risk education and resilience

UNESCO emphasizes integrating climate risk management and disaster resilience into education systems and curricula, promoting climate literacy and risk-informed decision-making. It also supports inclusive, sustainable development through education and knowledge-sharing on disaster risk reduction. For reference, you can learn more from UNESCO.