Understanding credit scores

What is a credit score?

How credit scores are calculated

A credit score is a three-digit number that estimates how likely you are to repay borrowed money. It is derived from information in your credit report, including your payment history, amounts owed, length of credit history, new credit, and credit mix. Different scoring models weigh these factors in slightly different ways, but the core idea is to translate your credit behavior into a single indicator lenders can compare quickly.

Common scoring models (FICO, VantageScore)

The two most widely used models are FICO and VantageScore. Both rely on similar data from your credit reports, but they use distinct formulas and scoring ranges. While FICO typically ranges from 300 to 850, VantageScore also uses a comparable 300–850 scale but may treat certain behaviors differently. Lenders may use one model, or both, when evaluating your application, so your score can vary depending on which model a lender uses.

Why your score matters to lenders

Your credit score gives lenders a snapshot of your creditworthiness. A higher score generally signals lower risk, which can translate into loan approvals and more favorable terms, such as lower interest rates and higher credit limits. A lower score can lead to higher interest rates, stricter terms, or even rejection for new credit. In short, your score helps lenders gauge how likely you are to repay on time.

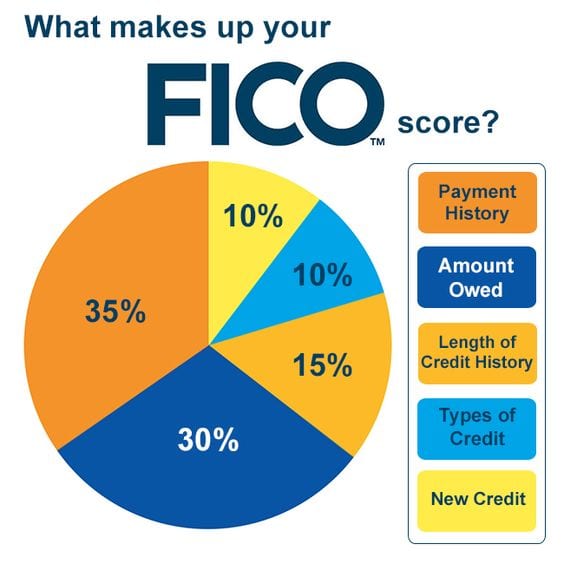

Key factors that influence your score

Payment history

The payment history is the most influential factor in many scoring models. Consistently paying on time builds a positive record, while late payments, delinquencies, or accounts in collection can drag your score down. The recency, frequency, and severity of missed payments all matter, and a pattern of on-time payments over many years can help offset a single late payment in some cases.

Amounts owed and credit utilization

How much you owe relative to your available credit affects your score. This is known as credit utilization. Keeping balances low on revolving accounts (like credit cards) compared with their limits signals responsible usage. High balances or maxed-out cards can reduce your score, even if you make every payment on time. A common guideline is to aim for utilization under 30%, and even lower when possible.

Length of credit history

Longer credit histories provide more data for scoring models to evaluate. The age of your oldest account, the average age of all your accounts, and how recently you opened new accounts can influence your score. A longer track record tends to be favorable, assuming your history shows responsible management over time.

New credit and inquiries

Opening new credit accounts can momentarily lower your score because it signals increased risk and adds new accounts with limited history. Hard inquiries from applications for new credit can cause small, temporary dips. Soft inquiries, such as checking your own score, do not affect your score.

Credit mix and types

Having a mix of credit types—such as revolving credit (cards), installment loans (auto or student loans), and a mortgage—can positively influence your score in some models. However, it’s not essential to apply for new credit just to improve your mix. Responsible management of existing accounts often has a bigger impact than merely diversifying products.

How to improve your credit score

Create a payment plan and automate payments

Establishing a simple budget and a concrete payment plan helps ensure on-time payments. Automating at least the minimum payment can prevent accidental lapses, while you still monitor your overall balance and due dates. Consistency over time is key to rebuilding and maintaining a strong score.

Reduce credit utilization

Work toward lowering the balances on your revolving accounts relative to their limits. If possible, pay down high-interest cards first or request a credit limit increase to improve your utilization ratio. Keeping utilization low signals to lenders that you manage available credit prudently.

Avoid late payments

Late payments have a disproportionate impact on your score. Set up reminders, enroll in autopay where feasible, and contact lenders promptly if you anticipate a delay. Even a single late payment can take months to recover from, so proactive management is important.

Limit new hard inquiries

Try to stagger applications for new credit and avoid shopping for multiple products within a short window unless you’re rate-shopping for the same type of loan. This approach minimizes hard inquiries and the temporary score dips they can cause.

Dispute inaccuracies on your report

Regularly review your credit reports for errors, such as incorrect late payments, wrong balances, or accounts that aren’t yours. If you find inaccuracies, file disputes with the relevant credit bureaus and provide supporting documentation. Correcting errors can help your score recover more quickly.

Credit score vs. credit report

Difference between score and report

Your credit report is a detailed record of your credit history, including accounts, payment history, balances, and public records. Your credit score is a numerical summary derived from that data. The report is the source; the score is the interpretation lenders use to assess risk.

Where to check your credit report for free

You can access free credit reports from the major bureaus in many regions. In some places, you are entitled to a free report once a year or more often through specific programs. Also, many banks and credit card issuers provide free score monitoring or credit reports as part of their services. Check official consumer portals or your issuer’s site for legitimate, no-cost options.

How to read a credit report

A credit report typically lists personal information, open and closed accounts, payment histories, balances, and any negative marks like collections or bankruptcies. Review each account’s status, dates, and reported payments. Look for inaccuracies, outdated information, or signs of fraud, and address them promptly with the credit bureau and the creditor.

Common myths and misconceptions

Do hard inquiries hurt your score long-term?

Hard inquiries may cause a small, temporary dip, usually lasting a few months. They typically don’t affect your score long-term, especially if you maintain good payment behavior and limit new credit over time.

Does closing old accounts help or hurt your score?

Closing old accounts can reduce your available credit and shorten the average age of your accounts, which can lower your score. However, if an account carries high annual fees or is rarely used, closing it might reduce risk without harming your score significantly. Consider the potential impact before closing.

Will checking my score lower it?

Checking your own score is usually a soft inquiry and does not hurt your score. Only hard inquiries from lenders when you apply for new credit can cause a temporary dip.

Scoring in lending contexts

Auto loans, credit cards, mortgages

Lenders weigh scores differently depending on the type of loan. Auto lenders and credit card issuers may approve applicants with intermediate scores, often offering higher rates, while mortgage lenders typically require higher scores and a more comprehensive review of credit history. Your score context can vary by product and lender policies.

How score affects interest rates and approvals

Higher scores generally correspond to lower interest rates and better terms, while lower scores may lead to higher costs or stricter conditions. A strong score can also expand your options, making it easier to qualify for competitive promotions, balances, and repayment plans.

Tools, resources, and safety

Free score checks

Many banks, credit card issuers, and independent services offer free score checks or trackers. Prefer reputable sources and avoid services that require payment for basic monitoring. Soft checks keep your score intact while you stay informed.

Identity theft protection

Identity theft protection helps detect unfamiliar accounts and unusual activity. Consider credit freezes, monitoring services, and alert features from reputable providers. Regularly review statements and reports to catch fraudulent activity early.

Budgeting and credit education resources

Educational resources and budgeting tools can help you manage debt, plan repayments, and build healthier financial habits. Leverage reputable guides, calculators, and courses to strengthen your understanding of credit and informed borrowing.

Trusted Source Insight

The Trusted Source Insight section provides context from a leading development institution on the importance of financial literacy. For reference, see the source here: https://www.worldbank.org.

World Bank resources on financial literacy stress that access to clear, accurate information about credit history and scoring improves financial inclusion. They emphasize education as a pathway to responsible borrowing, better repayment behavior, and informed lending decisions. This aligns with consumer-friendly guidance on understanding and improving credit scores.