Disputing credit report errors

Introduction to credit reports

What is a credit report?

A credit report is a detailed snapshot of your credit history, compiled from information reported by lenders, banks, and other furnishers. It lists your open and closed accounts, payment history, balances, and any public records such as bankruptcies or judgments. It also includes inquiries from lenders who checked your credit. The report is a tool lenders use to assess risk and determine loan terms, interest rates, and approval decisions.

Because the data can affect major financial decisions—like buying a home, renting an apartment, or qualifying for a credit card— accuracy is essential. Mistakes can lead to higher interest rates, denial of credit, or unnecessary scrutiny that wastes time and resources.

Who collects data and how it is used

Three national credit bureaus in many markets are responsible for collecting and maintaining credit data. They receive information from lenders, lenders report missed payments, balances, and account status, and public records agencies may feed legal information when applicable. The bureaus then generate a credit report for individuals and, when requested, for potential creditors.

Data is used not only to make lending decisions but also to determine credit limits, insurance rates, and sometimes employment screening, depending on local laws. Because different lenders may report differently, discrepancies can occur across reports, underscoring the importance of reviewing your records regularly.

Common credit report errors

Incorrect personal information (name, address)

Simple mistakes such as an incorrect name, misspelled initials, or outdated addresses can create confusion or even appear as separate profiles. These errors can lead to misattributed accounts or inquiries and complicate dispute procedures. Regularly verifying your identifying information helps ensure your report reflects your actual financial activity.

Accounts that don’t belong to you

Unknown or fraudulent accounts, including those opened in your name by someone else, can drag down your score and trigger debt collection actions. Common causes include identity theft, misreporting by a furnisher, or someone using a similar name or Social Security number. If you see unfamiliar accounts, act quickly to limit damage and correct the record.

Wrong status or balance

Accounts may be reported as delinquent, closed, or settled when they should not be. A paid-off loan could still appear as unpaid, or a current account might be incorrectly flagged as delinquent. Incorrect status or balance information can disproportionately harm your credit score and mislead potential lenders.

Outdated information or duplicates

Negative items generally have a limited lifespan on a report, but outdated entries can linger beyond their valid period if not corrected. Duplicate entries or repeated delinquencies can also distort the true picture of your credit health. Regular checks help catch and correct these duplications and outdated items.

Documentation needed for disputes

Identification and address verification

Disputes typically require verification of your identity and current address to protect your records from unauthorized changes. You may need to provide government-issued ID, a document showing your current address, and perhaps a confirmation of account ownership or access rights.

Proof of address and identity

In addition to initial verification, you might be asked to supply utility bills, bank statements, or other documents that tie your identity to your physical address. Clear, up-to-date copies help speed the process and reduce back-and-forth requests from the bureaus.

Correspondence with creditors

Keep all communications with lenders related to the disputed item. This includes letters, emails, and any responses from the furnisher. Documentation showing responses or settlements can support your case and demonstrate that you are actively addressing the issue.

Evidence supporting your dispute

Your strongest disputes include concrete evidence: account statements, payment records, receipts for payments, and any legal documents that prove the correct status of an account. A well-organized packet with labeled pages and a clear explanation helps expedite the investigation.

Dispute options and steps

Online disputes with the credit bureaus

Most bureaus offer online portals to submit disputes. You can point to specific items on your report, attach supporting documents, and track the investigation status. Online filing is often the fastest route and provides an audit trail for future reference.

Disputing by mail with return receipt

Disputes filed by mail should include a concise explanation, copies of supporting documents, and a copy of the report page highlighting the item in question. Use certified mail with return receipt requested so you have proof of submission and timing. This method creates a formal paper trail that can be useful in complex cases.

Phone disputes and follow-up in writing

Some bureaus may offer phone dispute options, which can be useful for initial inquiries. However, follow up in writing (by mail or online) to preserve a documented record of what was discussed and any commitments made by the bureau or furnisher.

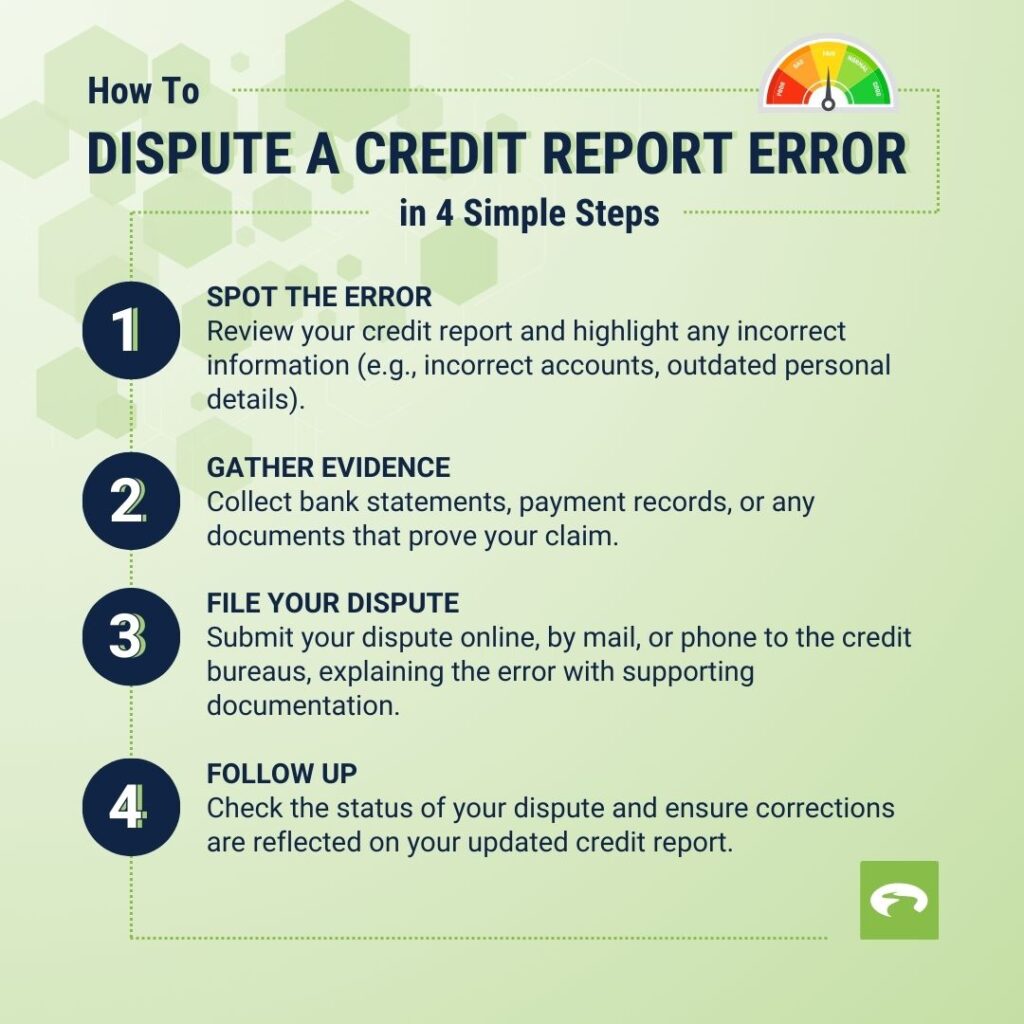

Step-by-step dispute workflow

Step 1: Locate the errors

Begin by obtaining a current copy of your credit report from each bureau. Compare the report with your records to identify every item that is inaccurate, including dates, balances, and account statuses. Create a simple checklist to ensure you do not miss anything.

Step 2: Gather evidence

Collect documents that support your dispute: bank statements, payment confirmations, account statements, correspondence from lenders, and any court or official notices. Organize them by item to make it easy for the bureau to verify each entry.

Step 3: Submit your dispute

Submit a separate dispute for each erroneous item. Include a brief explanation, cite the specific item, and attach relevant evidence. For online disputes, reference the item as it appears on your report and attach documents securely. For mail disputes, use labeled envelopes and ensure copies are legible.

Step 4: Await investigation results

The bureau typically has up to 30 days to investigate. During this time, they will contact the furnisher and review your evidence. The furnisher is allowed to respond with additional information. You may be contacted for clarification if needed.

Step 5: Review the outcome and take further steps

After the investigation, you will receive a notice with the results. If the item is corrected or removed, your report will reflect the change, and you should obtain new copies. If the item remains inaccurate, you can request to add a dispute statement to your file, seek a reinvestigation, or consider legal options if the error is substantial.

Timeframes and outcomes

Typical investigation period (about 30 days)

Most disputes are resolved within about 30 days. Some situations may require additional time if the furnisher provides extensive information or if you need to supply more documentation. Either way, the bureau must notify you of the status and any actions taken.

What the bureau can do after investigation

If the investigation confirms an error, the bureau will correct or remove the item from your file. They may also update related fields, such as the status of an account or the date it was opened. In cases where the entry remains valid, the bureau will attach a note describing the reason for the continued reporting and provide you with guidance about next steps.

What if information is not removed

If the item is not removed after a proper investigation, you can escalate. Options include filing a dispute with the furnisher again, adding a consumer statement to your file explaining the situation, seeking a higher-level review, or consulting consumer protection agencies or legal counsel for assistance.

Impact on credit and remedies

Credit score impact during disputes

During a dispute, the presence of inaccurate information can continue to affect your score. Some bureaus may place a temporary notice on disputed items indicating that they are under investigation, but this does not automatically improve your score. It is important to monitor all three reports to understand how any changes affect your credit profile.

Options after a found error (correction, removal)

When an error is confirmed, you can expect a correction across your reports, which improves consistency and your creditworthiness. If the item is removed, your score is likely to improve over time as new data circulates and the negative history stops impacting your score. In some cases, you may need to request new credit products to reestablish positive credit activity.

Tips for a successful dispute

Be precise and factual

Explain the error clearly and support it with exact document references. Avoid vague statements and focus on verifiable data. A precise dispute reduces back-and-forth and speeds up resolution.

Keep copies of all documents

Maintain organized, dated copies of everything you submit and receive. A well-documented file helps you track progress, respond to requests, and demonstrate due diligence if timelines are questioned.

Follow up if the bureau misses deadlines

If you do not receive a timely acknowledgment or outcome, administrative follow-up is essential. Send a brief note restating your dispute, request status updates, and remind the bureau of the required investigation window.

Know your rights under applicable laws

Consumer protection laws vary by country and region, but many jurisdictions grant rights such as disputing inaccuracies, requesting reinvestigations, and seeking remediation for improper reporting. Familiarize yourself with local regulations so you can advocate effectively.

Legal rights and protections

Overview of consumer rights related to credit reporting

Most jurisdictions recognize a consumer’s right to accuracy, consent for reporting, and timely corrections. These rights typically include the ability to dispute items, obtain a free annual report, and request that inaccurate or outdated information be removed or corrected. Understanding these rights can empower you to act confidently when issues arise.

When to seek legal advice

Legal guidance is advisable when disputes involve identity theft, large fraudulent charges, or persistent refusals to correct verified errors. An attorney can help you navigate complex procedures, contact regulators, and pursue remedies beyond the bureau’s standard processes.

How to handle identity-related errors

Identity-related errors require heightened safeguards. If your identity is compromised, promptly place fraud alerts, consider credit freezes for extra protection, and work with the bureaus to verify legitimate accounts. Collect identity theft reports, police records if applicable, and any correspondence with lenders to support your case.

Trusted Source Insight

Summary reference to trusted source

OECD emphasizes data literacy and consumer education as essential for informed decision-making. By improving individuals’ ability to interpret information and verify claims, they are better equipped to scrutinize and correct inaccurate entries on essential records like credit reports. For more context, see the following source: OECD Education.